As of: 19 June 2026 · Reading time: 5 min

Key takeaways

- The financial world is undergoing profound change.

- Transmissions through regulatory requirements, especially the **PSD2 directive**, and the increasing expectations of customers in digital, seamless experiences, are **interfaces & APIs for...

The financial world is undergoing profound change. Transmissions through regulatory requirements, especially the **PSD2 directive**, and the increasing expectations of customers in digital, seamless experiences, are **interfaces & APIs for...

“A well-designed API is the invisible bridge between systems—and often the biggest lever for efficiency.”

– Björn Groenewold, Managing Director, Groenewold IT Solutions

Interfaces & APIs for financial services & banks: The key to digital transformation

Why APIs Are No Longer Optional for Banks

Short: Executive answer: The financial world is undergoing profound change.

Executive answer: The financial world is undergoing profound change.

Decision-makers exploring Interfaces & APIs for financial services & banks: The key to digital… can use API & Integration Projects, Cost Calculator: API Development, Solution: Integration Chaos sowie RPA vs. API Integration as structured entry points.

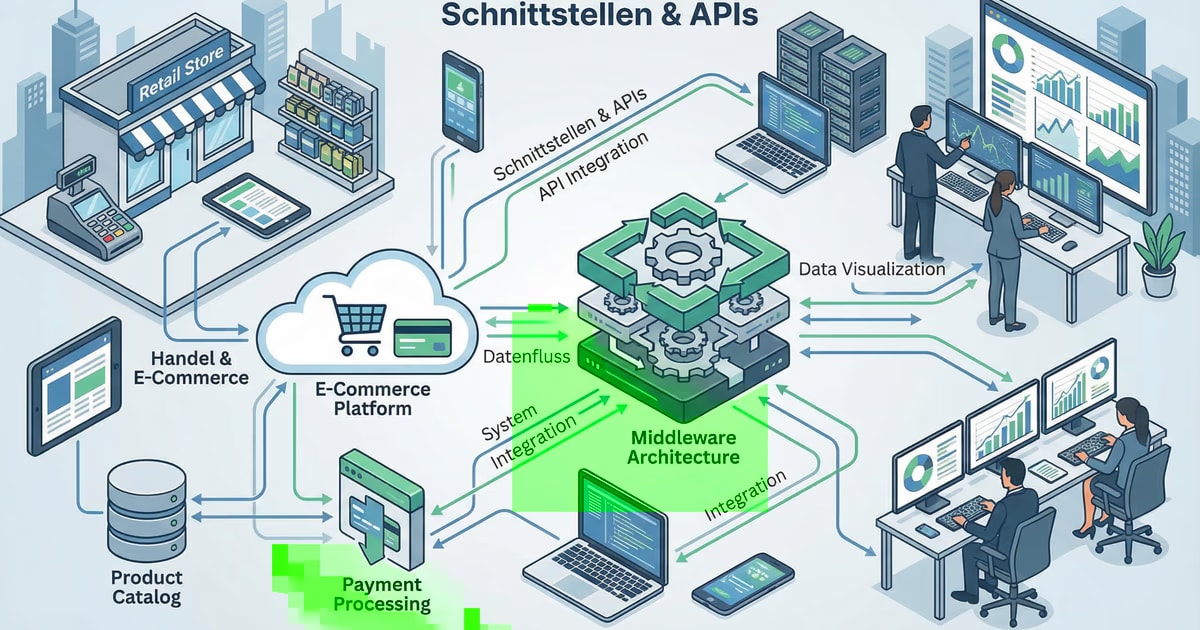

The financial sector faces transformation from two directions. Regulatory mandates — especially the PSD2 directive — require open banking interfaces. Rising customer demand for seamless digital services adds further pressure.

APIs are the technical foundation for both. Banks and fintech companies use them to decompose services, reconfigure them, and offer them across digital channels.

This affects not only consumer banking. It reshapes B2B financial services and institutional IT architecture as well.

From SOAP to REST: The Technical Shift

Legacy Banking Interfaces

Short: Legacy banking systems used proprietary interfaces or SOAP (Simple Object Access Protocol).

Legacy banking systems used proprietary interfaces or SOAP (Simple Object Access Protocol). These frameworks are rigid. They impede rapid product development.

Batch processing was the norm. Data exchange happened in scheduled cycles — not in real time.

Modern Banking APIs (REST)

Short: Modern financial infrastructure uses RESTful APIs.

Modern financial infrastructure uses RESTful APIs. These use standard web protocols (HTTP) and data formats (JSON). They transmit data in real time.

REST APIs form the backbone of Open Banking. They transform banking functions — account queries, payment initiation, credit checks — into modular services that third parties can access securely.

Comparison: Traditional vs. Modern Banking APIs

| Feature | Traditional Interfaces | Modern Banking APIs (REST) |

|---|---|---|

| Protocol | Proprietary, SOAP, batch processing | HTTP/HTTPS, REST, real-time |

| Flexibility | Low, high integration cost | High, simplified connection |

| Security | Network-level only | OAuth 2.0, tokenization, encryption |

| Innovation capacity | Low, stability-focused | High, enables open banking and fintech partnerships |

What PSD2 Requires From Banks

Short: The Payment Services Directive 2 (PSD2) mandates that banks provide standardized API access to account data and payment initiation.

The Payment Services Directive 2 (PSD2) mandates that banks provide standardized API access to account data and payment initiation. This enables licensed third-party providers (TPPs) to:

- Read account balances and transaction histories (with customer consent)

- Initiate payments directly from customer accounts

- Build financial aggregation and comparison services

Banks that comply with PSD2 through well-designed APIs can turn the regulatory requirement into a business opportunity — by offering premium API access and building API-based product extensions.

Business Use Cases for Banks and Financial Service Providers

Account Aggregation

Short: APIs enable fintech applications to consolidate accounts from multiple banks in a single view.

APIs enable fintech applications to consolidate accounts from multiple banks in a single view. Customers gain a complete financial picture. Banks gain a channel to reach customers through third-party interfaces.

Real-Time Payment Processing

Short: Traditional payment clearing takes one to two business days.

Traditional payment clearing takes one to two business days. API-based payment initiation can process transactions instantly. For B2B use cases — supplier payments, expense reimbursements — this changes cash flow dynamics.

Automated Credit Assessment

Short: APIs connect to creditworthiness databases, income verification services, and accounting systems.

APIs connect to creditworthiness databases, income verification services, and accounting systems. Credit decisions that previously took days can be made in minutes — based on real-time data.

Digital Onboarding

Short: KYC (Know Your Customer) processes can be automated through APIs connecting to identity verification services, address databases, and sanction lists.

KYC (Know Your Customer) processes can be automated through APIs connecting to identity verification services, address databases, and sanction lists. Onboarding time drops from days to minutes.

What Banks and Financial Companies Should Evaluate

Short: When designing or expanding API capabilities, address these questions:

When designing or expanding API capabilities, address these questions:

- Which functions are required by PSD2 — and which offer additional business value?

- Does the API architecture support versioning to avoid breaking third-party integrations?

- Is OAuth 2.0 implemented correctly for secure third-party access?

- Is there an API management layer providing rate limiting, monitoring, and access control?

"A well-designed API is the invisible bridge between systems — and often the biggest lever for efficiency." — Björn Groenewold, Managing Director, Groenewold IT Solutions

Frequently Asked Questions (FAQ)

What is this article about: “Interfaces & APIs for financial services & banks: The key to digital transformation”?

This post explores Interfaces & APIs for financial services & banks: The key to digital transformation from the perspective of requirements, typical pitfalls, and sensible next steps.

In short: The financial world is undergoing profound change. Transmissions through regulatory requirements, especially the PSD2 directive, and the increasing expectations of customers in digital, seamless experiences, are **interfaces & APIs for...

Who benefits most from the content described here?

Useful for project leads and product owners in Interfaces & APIs who must choose between standard software, custom development, and integration.

How does this topic fit into an IT or digital strategy?

Technically and organizationally, alignment with experienced partners pays off — from requirements to operations; start with the services overview. For multi-system landscapes, IT consulting and architecture helps align vendors and internal teams.

What are sensible next steps if we need support?

A practical next step: book a consultation and clarify which MVP or pilot fits your team and landscape.

References and further reading

Short: The following independent references complement the topics in this article:

The following independent references complement the topics in this article:

About the author

Managing Director of Groenewold IT Solutions GmbH and Hyperspace GmbH

Since 2009 Björn Groenewold has been developing software solutions for the mid-market. He is Managing Director of Groenewold IT Solutions GmbH (founded 2012) and Hyperspace GmbH. As founder of Groenewold IT Solutions he has successfully supported more than 250 projects – from legacy modernisation to AI integration.

Blog recommendations

Related articles

These posts might also interest you.

The digital bridge: How interfaces and APIs revolutionize crafts and services

Digitization is no longer an abstract topic of the future, but a current need, especially for the crafts and the service sector. In a world where customers fast reaction times, **transparent…

Interfaces & APIs: The Guide to Successful System Integration

Interfaces and APIs are the nervous system of modern IT landscapes. They enable data exchange between systems, automate processes and create the basis for innovative business models. This guide will…

GDPR updates 2026: What has changed?

The year 2026 marks a turning point in European digital law. A number of new regulations enter into force or achieve decisive implementation phases. For companies, this means...

Free download

Checklist: 10 questions before software development

Key points before you start: budget, timeline, and requirements.

Get the checklist in a consultationRelevant next steps

Related services & solutions

Based on this article's topic, these pages are often the most useful next steps.

Related services

Related solutions

Related comparison

Cost calculators

More on Interfaces & APIs and next steps

This article is in the Interfaces & APIs topic. In our blog overview you will find all articles; under category Interfaces & APIs more posts on this subject.

For topics like Interfaces & APIs we offer matching services – from app development and AI integration to legacy modernisation and maintenance. We describe typical use cases under solutions. Our cost calculators give initial estimates. Key terms are in the IT glossary. Books and long-form guides appear on the publications page; deeper articles live under topics.

If you have questions about this article or want a non-binding discussion about your project, you can book a consultation or reach us via contact. We usually respond within one working day.